Here’s my forecast: “The global economy is going to have a significant downturn and record levels of debt are going to make it worse.” Sound scary enough? Put it in the headline and I can be assured of lots of clicks! I might even be called a deep thinker! The problem is that there is nothing new or profound in this. A significant economic downturn is inevitable at some point (it’s just the economic cycle), debt problems are involved in most economic downturns and such calls are a dime a dozen.

A standard scare now is that memories of the role of excessive debt in contributing to the GFC have worn thin and total global debt has pushed up to a new record high of over $US200 trillion – thanks largely to public debt in developed countries (with more to come in the US as Trump’s fiscal stimulus rolls out), Chinese debt and corporate debt (and household debt in Australia of course). Also, that its implosion is imminent and inevitable as interest rates normalise and that any attempt to prevent or soften the coming day of reckoning will just delay it or simply won’t work. However, in reality it’s a lot more complicated than this. This note looks at the main issues.

Global debt – how big is it and who has it?

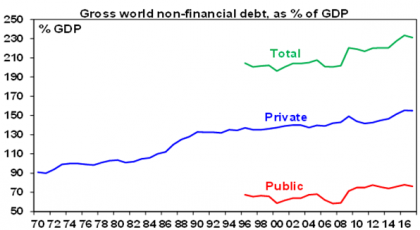

Total gross world public and private debt is around $US171 trillion. Adding in financial sector debt pushes this over $US200 trillion but that results in double counting. Either way it’s a big and scary number. But it needs to be compared to something to have any meaning or context. A first point of comparison is income or GDP at an economy wide level. And even here new records have been reached with gross world public and private non-financial debt rising to a record of 233% of global GDP in 2016, although its fallen fractionally to 231% since. See the next chart.

Source: IMF, Haver Analytics, BIS, Ned Davis Research, AMP Capital

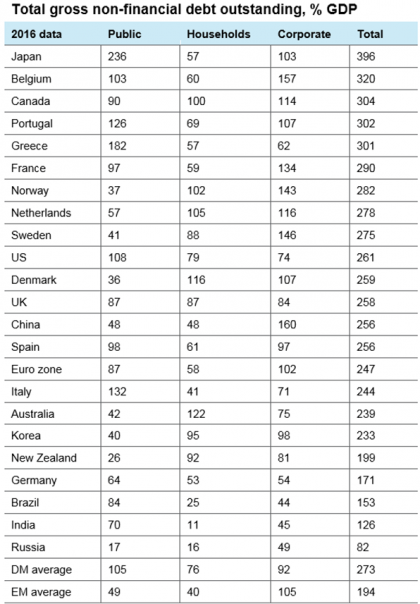

The next table compares total debt for various countries.

Source: IMF, Haver Analytics, BIS, Ned Davis Research, AMP Capital

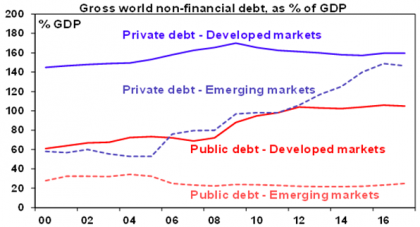

The next chart shows a comparison of developed world (DM) and emerging world (EM) debt – both public and private.

Source: Haver Analytics, BIS, Ned Davis Research, AMP Capital

It can be seen that the rise in debt relative to GDP since the GFC owes to rising public debt in the developed world and rising private debt in the emerging world. Within developed countries a rise in corporate debt relative to GDP has been offset by a fall in household debt, so private debt to GDP has actually gone down slightly. And a rapid rise Chinese debt (particularly corporate) has played a role in the emerging world.

Of course, it needs to be mentioned that measures of gross debt exaggerate the total level of debt. For example, because of government holdings of debt instruments via sovereign wealth funds, central bank reserves, etc, net public debt is usually well below gross debt. In Norway net public debt is -91% of GDP and in Japan it’s 153% of GDP. But as an overview:

-

Japan, Belgium, Canada, Portugal and Greece have relatively high total debt levels;

-

Germany, Brazil, India and Russia have relatively low debt;

-

Australia does not rank highly in total debt – it has world-beating household debt but low public & corporate debt;

-

Emerging countries tend to have relatively lower debt, but rising private debt needs to be allowed for particularly in China, where corporate debt is high relative to GDP.

The bottom line is that global debt is at record levels even relative to GDP so it’s understandable there is angst about it.

Seven reasons not to be too alarmed about record debt

However, there are seven reasons not to be too alarmed by the rise in debt to record levels.

First, the level of debt has been trending up ever since debt was invented. This partly reflects greater ease of access to debt over time. So that it has reached record levels does not necessarily mean it’s a debt bomb about to explode.

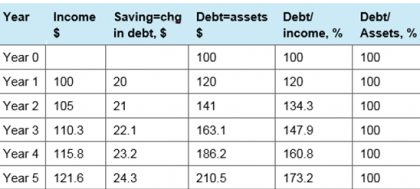

Second, comparing debt and income is a bit like comparing apples and oranges because debt is a stock while income is a flow. Suppose an economy starts with $100 of debt and $100 in assets and in year 1 produces $100 of income and each year it grows 5%, consumes 80% of its income and saves 20% which is recycled as debt and invested in assets. How debt, debt to income & debt to assets evolves can be seen in the next table.

Debt ratios over time

Source: AMP Capital

At the end of year 1 its debt to income ratio will be 120%, but by the end of year 5 it will be 173%. But assuming its assets rise in line with debt its debt to asset ratio will remain flat at 100%. So the very act of saving and investing creates debt and {% rising debt to income ratios. 1 China is a classic example of this where it borrows from itself. It saves 46% of GDP and this saving is largely recycled through banks and results in strong debt growth. But this is largely matched by an expansion in productive assets. The solution is to spend more, save less and recycle more of its savings via investments like equity.

Third, the rapid rise in private debt in the emerging world is not as concerning as they have a higher growth potential than developed countries. Of course, the main problem emerging countries face is that they borrow a lot in US dollars and either a sharp rise in the $US or a loss of confidence by foreign investors causes a problem. This has started to be a concern lately as the $US is up 7% from its low earlier this year.

Fourth, debt interest burdens are low and in many cases falling as more expensive, long maturity, older debt rolls off. And given the long maturity of much debt in advanced countries it will take time for higher bond yields to feed through to interest payments. In Australia, interest payments as a share of household disposable income are at their lowest since 2003, and are down by a third from their 2008 high. There is no sign of significant debt servicing problems globally or in Australia.

Fifth, most of the post GFC debt increase in developed countries has come from public debt & governments can tax and print money. Japan is most at risk here given its high level of public debt, but borrows from itself. And even if Japanese interest rates rise sharply (which is unlikely with the BoJ keeping zero 10-year bond yields with little sign of a rise) 40% of Japanese Government bonds are held by the BoJ so higher interest payments will simply go back to the Government.

Sixth, while global interest rates may have bottomed, the move higher is very gradual as seen with the Fed and the ECB, Bank of Japan and RBA are all a long way from raising rates. What’s more, central banks know that with higher debt to income ratios they don’t need to raise rates as much to have an impact on inflation or growth as in the past.

Finally, debt alone is rarely the source of a shock to economies. Broader signs of excess such as overinvestment, rapid broad-based gains in asset prices and surging inflation and interest rates are usually required and these aren’t evident on a generalised basis. But these are the things to watch for.

Concluding comment

History tells us that the next major crisis will involve debt problems of some sort. But just because global debt is at record levels and that global interest rates and bond yields have bottomed does not mean a crisis is imminent. For investors, debt levels are something to remain alert too – but in the absence of excess in the form of booming investment levels, surging inflation and much higher interest rates, for example, there is no need to be alarmed just yet.

1.↩ [My favourite example of the complex relationships between income, saving and debt came from Bank Credit Analyst Research. Suppose there is an island with 100 people, each making 100 coconuts a year. Here’s three possibilities.

Case 1: Output is 10,000 coconuts with each person consuming 100. Saving and investment are zero and no debt is created.

Case 2: Each person consumes only 75 coconuts a year, selling the remainder to a plantation who buys them with a bank loan and plants them resulting in 2500 new coconut trees. Consumption is 7500 coconuts. Savings and investment are 2500 and debt has gone up by 2500 coconuts.

Case 3: Each person consumes 125 coconuts, by importing 25 each from foreign islands. Consumption is now 12,500 coconuts, savings is -2500 coconuts, investment is zero and the current account deficit is 2500. External debt goes up by 2500. This gets risky if the other islands want their coconuts back!

So debt can rise even if an economy lives within its means & invests for the future. ]↩

Source: AMP Capital 19 June 2018

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.