Australia’s love of home ownership can lead real estate investors to overlook the potential benefits of global listed real estate and owning a share of some of the best real estate assets in the world.

Most investors understand the benefits of listed real estate. It has higher liquidity and lower transaction costs than direct property.

But there are three lesser known benefits of listed real estate that may make it suitable for investors seeking income.

1. Attractive risk-adjusted returns

The first is attractive risk-adjusted returns. Given close to 60% of the asset class is in North America, therefore using US data as a proxy, for investors in that jurisdiction willing to hold listed real estate for five years or more1 , listed real estate has the potential to generate similar returns, and the same diversification benefits to a portfolio over time, as physically owning the actual buildings. However we’d note that there may be more shorter term volatility as shown in Figure 1, but that is to be expected as you can find daily liquidity for an illiquid asset class.

Many investors equate listed real estate with equities and view it as a short-term investment. But the asset class hits its stride when held over time. Real estate, both listed and direct, is a long-term investment by the very nature of the leasing contracts and the longevity of the physical assets.

The correlation of returns between listed and unlisted increases significantly as the investment horizon lengthens. Indeed, the correlation between the two is 0.9 of listed share prices and the underlying real estate valuations of the assets they own on a rolling three year basis (figure 1 is the US)2, if you remove leveraging differences from both asset classes and control them for the industry practice of appraisal smoothing.

Figure 1 – Rolling Three Year Annualised Total Return: Listed Shares & Underlying Real Estate Assets – USA

Source: Green Street Advisors – December 2018

2. Direct property beacon

We believe that listed real estate trusts (REITS) can also be used by investors to determine what the direct market is likely to do. Again using the US as a proxy, when analysing US data of whether REITs are trading at a premium or discount to net asset value (NAV) – the value of the trust’s holdings at a given time — has historically been an indicator in that jurisdiction of how the direct market will move in the coming 12 -18 months, although future performance can never be guaranteed.

Put very simply, if a REIT trades at a premium to its NAV, the market believes its assets will appreciate above levels indicated by market pricing of the underlying direct real estate. The inverse occurs when trading at discounts.

When REITs in the US have traded at NAV discounts greater than 10 per cent, historically they have subsequently outperformed the unlisted market by more than 1200 bps per annum over the next three years. Observed NAV premium/discounts in the public market provide a strong signal as to the appropriate mix of listed vs unlisted real estate, and there have been times in the past when investors with no listed exposure have experienced suboptimal performance.

Figure 2 – Listed Premiums/Discount and unlisted returns

Source: Green Street Advisors – March 2018

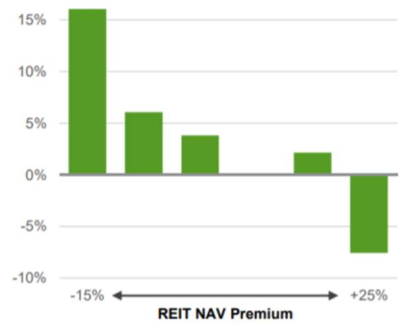

Figure 3 – Listed Returns minus unlisted returns, next 3 years (Ann.)

Source: Green Street Advisors – March 2018

3. Global Appeal

The third characteristic is the growing global appeal of listed real estate.

Listed real estate was once the poster child of leverage, particularly in Australia during the financial crisis. But that was now a decade ago and many lessons have been learned and now listed real estate has resumed the role for which it was intended: a proxy for direct real estate at a point in time when allocations to real estate as an asset class are rising.

Globally, in many markets, listed real estate is trading at a discount to NAV. The biggest discounts are in Japan developers, retail and the UK and New York office markets. Australian REITs, with the exception of retail malls, are trading at a premium, with larger premiums ascribed to fund managers, industrial and datacentre landlords.

In individual markets where listed real estate is trading at a discount to NAV, the best management teams have been taking advantage of strong pricing in direct real estate markets, selling core assets and using the proceeds to either pay down debt or return capital to investors.

Listed real estate can be a complement to unlisted property or a useful proxy for unlisted property. This is particularly the case for investors who want to establish an allocation to real estate but are struggling amid global competition for quality assets and don’t want the headache or complexity of managing direct property assets. The AMP Capital Core Property Fund has allocations to both listed and unlisted real estate.

Greater diversification

On top of these benefits, global listed real estate typically has deep and unrivalled access to a greater diversity of institutional quality real estate sectors than the unlisted market. These sectors may include (but are not limited to) last mile logistics, datacentres, healthcare, aged care and manufactured housing.

These different sectors perform under varying economic conditions and their relevance and portfolio sizing should be assessed on what role they play in the underlying economy of the future. Given many of them are intertwined with long-term secular economic trends, having exposure to these assets is more logical to us than owning a retail dominated fund or a residential apartment investment.

Risks of investing in listed real estate

As with all investments there are associated risks to be aware of. Risks specific to real estate investments include the risks of investing in share markets, property and international markets, as well as the risks associated with interest rates, gearing and the cost of debt, derivatives, investment management, co-ownership of assets, fluctuations in rental income, rental demand and fund termination risks. For more information of the risks of investing in these types of assets, investors should consult the offer documents for the fund.

1Source: Green Street Advisors (Feb 2016)

2Source: Green Street Advisors (Dec 2018)

Investors should consider the Product Disclosure Statement (PDS) available from AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) (AMP Capital) for the AMP Capital Core Property Fund (Fund)) before making any decision regarding the Fund. The PDS contains important information about investing in the Fund and it’s important investors read the PDS before making a decision about whether to acquire, continue to hold or dispose of units in the Fund. The Trust Company (RE Services) Limited (ABN 45 003 278 831, AFSL 235150) (The Trust Company), a wholly owned subsidiary of The Trust Company Limited (ABN 59 004 027 749), is the responsible entity of the Fund and the issuer of units in the Fund. The Trust Company has not prepared this information and makes no representation or warranty as to the accuracy or completeness of any statement in it. Neither The Trust Company nor any company in the AMP Group (which includes AMP Capital and AMPCFM) guarantees the repayment of capital or the performance of any product or any particular rate of return referred to in this document. Past performance is not a reliable indicator of future performance. While every care has been taken in the preparation of this document, AMP Capital makes no representation or warranty as to the accuracy or completeness of any statement in it including without limitation, any forecasts. This information has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. Investors should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.

Author: James Maydew, BSc (Hons), MRICS, Head of Global Listed Real Estate, Sydney, Australia

Source: AMP Capital 11 July 2019

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.